Infrastructure Funds… Why do These Exist Again?

When the trendiest investment product on the block doesn’t deliver

As an investor you have two levers you can traditionally manipulate to produce a desired portfolio of investments: risk and return. In the world of finance, returns are often defined on an annual growth rate basis rather than in terms of absolute growth rates. For example, if an investment returned 100% in total over a 5-year period (i.e., you doubled your money in 5 years), we’d say that this investment produced a ~15% internal rate of return (IRR). More simply, you compounded your money at 15% / year for 5 years.

Risk, on the other hand, is defined in terms of the variance associated with those returns. Imagine you have two investments, A and B. Over a 5-year period investment A’s returns ranged between -5% and 10% whereas investment B’s returns ranged from -20% to 20%. We would consider B to be a “riskier” investment because the total variance in its returns was higher than A.1

When investors construct portfolios, they often treat these two variables like weights on either side of a barbell. You increase or reduce risk to “balance” the return profile of your investments. As such, investors (especially the large LPs we spoke about in my last post) are often allocating capital to a variety of investments to reach their target risk/return thresholds.

Recently, however, there’s another factor that’s begun to mix into this risk/return equation: ESG.

For those who are unfamiliar with what ESG is, here’s a quick primer:

Environmental, social, and governance (ESG) investing refers to a set of standards for a company’s behavior used by socially conscious investors to screen potential investments.

Environmental criteria consider how a company safeguards the environment, including corporate policies addressing climate change, for example. Social criteria examine how it manages relationships with employees, suppliers, customers, and the communities where it operates. Governance deals with a company’s leadership, executive pay, audits, internal controls, and shareholder rights.

As large asset managers are increasingly focused on painting (what I consider to be) a thin coat of “corporate social responsibility” over their investments (for more reading see this, this, and this), they’ve begun to consider the “impact” of a portfolio’s investments. As such, demand for “ESG-positive” investments and investment products have grown tremendously over the past decade. There is much to speak about regarding the efficacy of ESG as a measure of investment impact as well as numerous issues with how ESG measures are reported and analyzed, though these topics are to be explored in another discussion. Today, I’d like to focus on one of the pitfalls of ESG investing, the mischaracterization of ESG returns, though the lens of infrastructure funds.

Imagine you are a finance professional who owns a large private equity fund but are realizing (perhaps by reading my last post) that you have to drive investors to new products beyond your lagging flagship buyout fund. You might even be a proven real estate investor looking to develop new investment products for your LPs. As such, you look for opportunities to attract both ESG-oriented and low-risk profile investors to drive massive amounts of capital into your fund. You soon realize that you’re looking for an investment product that takes advantage of the following:

Long-time horizon projects with the ability to market them as driving social good

Assets in largely untapped (sometimes rural) areas that are relatively “stable” (aka slow growing) and previously untouched by the world of “high finance”

Industries which may receive significant amounts of federal subsidies in the near future, allowing for costly expansions to be partly funded by taxpayer dollars instead of private sector money

What combines all three of these criteria? Infrastructure investments. What defines an infrastructure investment? Think anything that reminds you of “unnecessary bureaucracy” or “poor customer service.” Examples include the following:

Broadband Providers & Datacenters (now defining the ever elusive and sexy category of “digital infrastructure”)

Real Estate

Utilities

Railways & Transportation

Renewable Energy

The value proposition for investing in these assets is something along the lines of the following:

These assets are extremely stable with little microeconomic sensitivity (put simply – your local utility provider isn’t going bankrupt anytime soon - unless… this happens - and such businesses are able to pass off cost increases to consumers in poor economic environments aka they’re “defensive”)

As such, from a “risk” / ”return” perspective infrastructure assets offer something which should sound too good to be true: large, stable cash flows with low risks associated with those cash flows

They provide investors with the ability to make “tangible social impact” by investing to improve a community’s infrastructure and, in theory, given their risk/return profile are able to be held for a long time horizon by private investors – affording them time to increase the efficiency of these assets through potential future investment

Sounds great, right? Not so fast… two things cannot be true at the same time:

Infrastructure investments are low risk

Infrastructure investments will produce private-equity-like returns

I’m not sure why investors haven’t realized this (perhaps its all in the name of appearing like they’re doing something on the ESG front), but infrastructure investments are perhaps riskier and less stable than we might initially think. Take the following two case studies as an example:

A Regional Utility Provider: Although such businesses may have stable revenues, they are subject to intense regulatory scrutiny. In addition, the amount of capital required to deploy additional services in new areas is enormous – resulting in reduced returns for an investor looking to implement any sort of growth strategy.

An EV battery production facility: Yes, businesses like this will fuel our energy transition; however, they will require significant investment today with the promise of profits tomorrow. This doesn’t work for infrastructure funds willing to take on 3-5 year time horizons in order to return capital to their LPs, as such assets like these are perhaps less stable than some investors might think

Once you do a little digging, you’ll soon realize that in order for infrastructure investments to produce returns both stable and large enough to benefit investors (after accounting for fees), these businesses have to be treated as private equity investments. This then transforms what seems to be a stable, low-risk asset class into one that is perhaps “stable,” but produces worse returns when compared to other investments of the same risk profile.

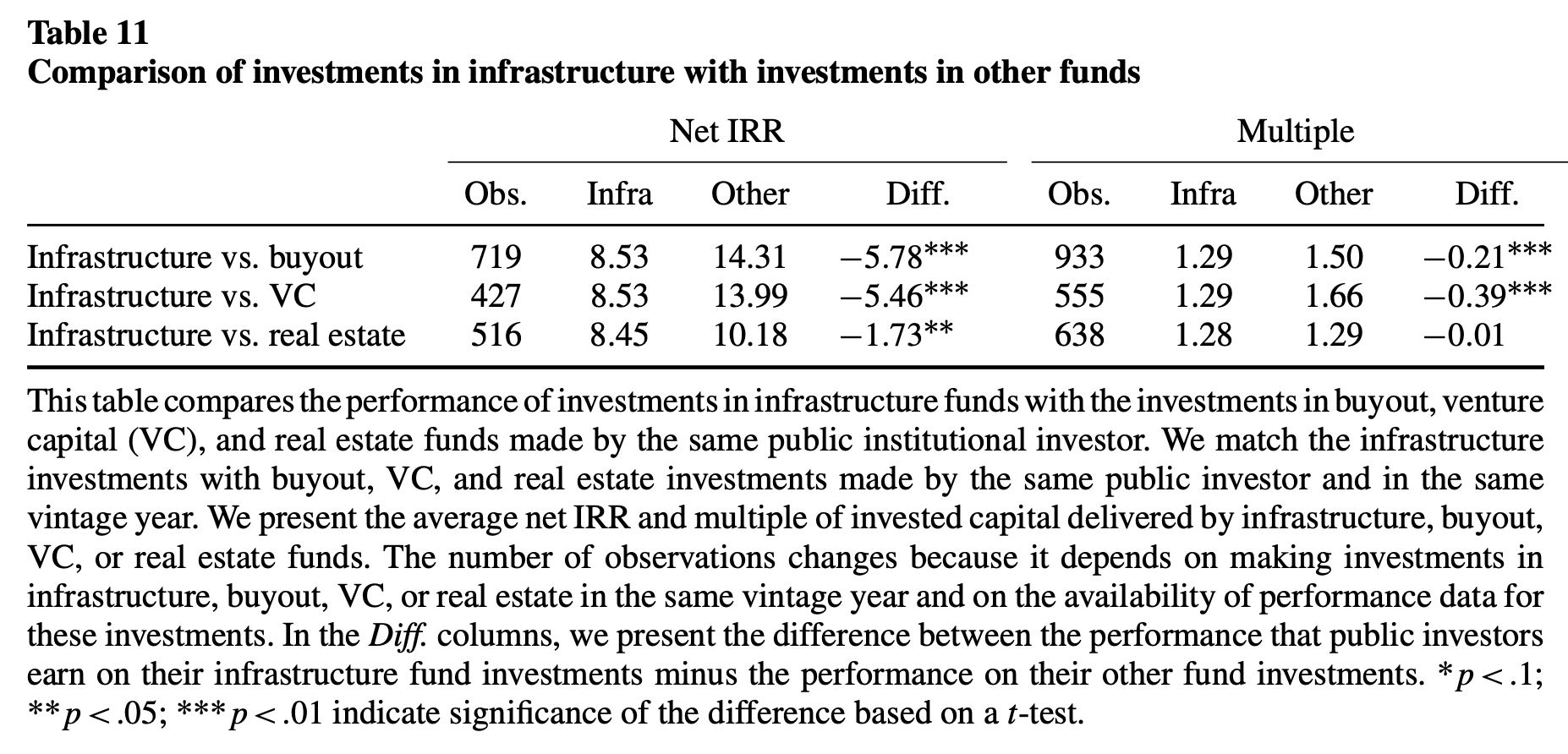

Researchers at Stanford’s business school have noticed this problem as well Professors Aleksandar Andonov, Roman Kraussl, and Joshua Rauh undertook an analysis of the performance of infrastructure funds asking this very question: Are infrastructure investments delivering the returns promised by their ever-growing appeal? (See their paper Institutional investors and Infrastructure Investing and this article)

The answer is, in short, no. See below excerpts and results from their analysis:

Institutional investors expect infrastructure to deliver long-term stable returns but gain exposure to infrastructure predominantly through finite-horizon closed private funds. The cash flows delivered by infrastructure funds display similar volatility and cyclicality as other private equity investments, and their performance similarly depends on quick deal exits…. ESG preferences and regulations explain 25%–40% of their increased allocation to infrastructure and 30% of their underperformance.2

Their research finds that, on average, infrastructure funds return more than 5% less than traditional PE funds while exhibiting similar amounts of risk for the same investments. Furthermore, such funds often return less than real-estate investments as well – an asset class which provides arguably better incremental upside and significantly more opportunities for diversification.

That said, it doesn’t seem like the growth of infrastructure funds is slowing anytime soon (link):

This means one of two will happen until something breaks:

The universe of quality infrastructure assets decreases and the number of funds bidding on these assets increases, thereby increasing the premiums firms pay for those assets and reducing returns for everyone

Infrastructure funds will transition to higher-risk, higher-reward investments at which point we’ll see these funds begin to market themselves as “ESG-oriented” private equity funds or remove any mention of ESG at all

And this is exactly what McKinsey’s research predicts, things are only going to get worse for infrastructure investors…

Time and again we see LPs being driven to allocate capital in ways that generate inefficiently distributed returns. Whether it be allocating to larger private equity funds with diminishing IRRs or infrastructure funds with poor risk/return profiles, one thing remains true: until LPs begin to move beyond whatever entrenched preconceptions they have about how to invest, the individuals whose funds are managed by those LPs will continue to suffer. That said, please don’t take this as investment advice 😊

For the next few posts we’ll move away from finance to explore topics related to the economics of education, elections, and other “more interesting” topics – subscribe and hop along for the ride.

As always, this is a simplified example but should illustrate enough to understand the rest of this piece.

Emphasis added for effect.